Over the past 17 years, we have witnessed the rapid development of new technologies and the swift creation of new markets. We have also learned that founders possess profound insights into their fields, often staying ahead of market trends. These insights, gleaned from our conversations with both new and established founders, significantly shape our investment strategies at Seedcamp.

Throughout the year, we engage in internal investment discussions about emerging technologies and cutting-edge research that have the potential to disrupt markets driven by strong tailwinds and/or rapid changes in market dynamics.

In this context, we rely on our founder relationships to guide us toward new and promising areas of investment exploration. While we approach these opportunities with a prepared mind, we recognise that our insights are no match for the expertise of the teams we support.

In this post, influenced by the trends and opportunities shared with us by founders and close angel friends, we present some of the investment team’s thoughts on sectors where there is a critical need for new solutions for both consumer and enterprise buyers.

We hope this list inspires prospective founders and angel investors with a glimpse of what excites us most in 2024. While we have some ideas about how incumbents in the areas highlighted might be disrupted, please note that this is not an exhaustive list of ideas or how companies might enter them.

In 2023, 91% of manufacturers re-optimised (some version of re-shoring) part of their production, up from just 7% in 2012. Coupled with an increasing workforce shortage and a generation of founders who cut their teeth at best-in-class, tech-enabled manufacturing companies like Tesla and Northvolt, we believe the next 12 months will be a very exciting time for manufacturing technology. We are especially excited about technology that removes data siloes, unearths operational insights, and enables digital twins that provide a holistic view of real world processes. Connecting IoT devices, forecasting productivity with better time-series modelling and simply improving centralised ledgers for factories are just some of what excites us.

Whilst some companies are tweaking existing factory processes, other models flip manufacturing on its head completely. Hadrian-esque software-orchestrated manufacturers can not only build a propriety operating system but also develop a fully connected factory from the bottom-up. We see a ton of potential for SMBs and multi-site manufacturers to deploy software and bring immense efficiency to their operations.

AI has dislodged long-standing inertia within traditional industries to adopt digital solutions. Leaders across shipping, agriculture, and heavy machinery are increasingly eager to collaborate with startups that can improve their productivity, reduce human error, and give their businesses a competitive edge. We’re excited to back founders who are helping these sectors automate repetitive tasks, on the field and in the back-office, and harness data for better decision-making. We’re especially looking forward to meeting with founders who are democratising this data and these insights for a wide range of employees, from the C-Suite and middle management to the individual contributor.

As we see rising safety and security provisions taking effect, our attention is not only turning to profitability-boosting but also to risk-mitigating solutions in the traditional economy. Whether through more streamlined audit processes in the shipping sector or improved workplace safety via off-the-shelf cameras on an oil rig, there is a pressing demand for technology to bridge the gap between the real and digital economy.

We think that it’s day one for the infrastructure that supports burgeoning enterprise data requirements. 90% of the world’s data was generated in the last three years and enterprises n better methods to ingest, transform, stream and analyse it. For example, streaming architecture is still nascent and there is limited consensus on how Flink, Kafka, Trino and Spark should be used in the enterprise and by whom; 75% of the Nasdaq use Kafka to stream only a fraction of their data.

Similarly, as ETL, ELT and reverse ETL have emerged, analysts have scrambled to store the freshly formatted data. However, databases and warehousing technologies are only just starting to move away from a model of one-size-fits-all. Hybrid transaction/analytical processing (HTAP) databases to run analytical and transactional processes, wide-columnDBs to load and search entire columns and navigationalDBs to store a physical location are in their first iterations. Each of these markets in themselves are enormous and deserve more than Postgres extensions to hack together solutions.

Databases continue to be an excellent enterprise insertion point because customers build applications on top of products they love (see Oracle). We can’t wait to see what the next generation of tooling will bring, especially as incumbents evolve from what started as customer-centric products to slow-innovating platforms and eventually to extractive pricing and contract lock-ins.

In 2023, Okta was hacked, phishing grew by 500-1000%, fraud cost enterprises $1 trillion globally and 90%+ of businesses with poor security practices missed revenue goals. It became very clear that in an AI-native world, existing architectures that permit human behaviour and detect anomalies with context, blind data packages are insufficient.

New security systems built from the bottom up are attracting our attention at Seedcamp. We are especially interested in protecting code as it is written, defending identity threats with next generation IAM, PAM and RBAC solutions, and preventing the leakage of data via the governance of foundation models, phishing detection and more. We’re actively looking for technology to combat our messy and unsecured digital environments and hand power back to the Chief Information Security Officer!

Healthcare systems across Europe and the US are under immense strain. Europe is experiencing a shortage of 2m healthcare professionals and in the UK alone 470K adults are waiting for care. This pressure is propelling AI into board-level hospital conversations at an unprecedented pace and 75% of health system executives believe generative AI has reached a turning point in its ability to reshape the industry. We are already seeing a high level of trust in co-pilot use cases, targeting administrative workflows (e.g. billing, clinical documentation, patient engagement). Clinical professionals are also starting to adopt tools that support in-flight procedures, although at a slightly slower rate. Computer vision to support procedure safety and accuracy or precision robotics to enhance the efficiency of operations are just two of the emerging areas we are most excited about.

We think that the next 10 years could witness astonishing change in how software can enhance the workflows, outputs, precision and personalisation of pharmaceutical and biological processes. Above all, we’ve been longtime believers in technology that sits at different intersections of the pharmaceutical lifecycle, from drug positioning to clinical trial development and approval. The time and cost to bring new drugs to market are still growing at a steep rate and we are excited about the role of software that can improve contract research, contract development and manufacturing to shortcut the sticking points on the ~10 year approval time horizon.

We think that this really is biology’s century; several foundation models for molecular discovery have emerged in Europe alone and data is increasingly shared across corporate and jurisdictional boundaries to encourage progress and collaboration. The Human Genome Project is just one example of what can be achieved and we are excited to see how research and development will weave in artificial intelligence but also quantum hardware to run compute-heavy simulations and nanotechnology to build with precision that was once impossible. Where once a data scientist would interact with software a few steps removed from operations at the lab bench, we are excited about the future of software built for scientists.

In 2023, we spent a lot of time with companies serving the residential and automotive energy market. As regulation comes into force in the mid and late 2020s regarding fuel consumption, EPC ratings and lots more, consumer upgrades facilitated by software are inevitable.

This year, we’re excited to explore industrial energy needs. Whether that’s figuring out how the grid can automatically rebalance with distributed batteries, or how to use sensors in a factory to understand and control energy consumption, we want to hear about it. Energy is highly contingent on hardware and the physical world across capture, transportation, and storage but new systems will work with the help of software that helps components seamlessly interact and connect resource availability with demand in real-time. Energy utilities are some of the most challenging businesses in the world — thin margins, regulated jurisdictions, and uncertain production create a lot of minefields and they may continue to face an uphill battle as procurement becomes more flexible and previously monopolised geographies become competitive.

In this space, we’re excited to meet founders working on the future of payments and authentication. It has been consensus for a short while that stablecoins can move money at faster speeds and cheaper rates than fiat currencies and that entities in countries who want protection from inflation or deflation, could benefit from an intuitive stablecoin platform. Companies like Fireblocks and Circle have become globally significant by providing walleting and on/off ramp infrastructure and we expect to see more companies that enable everyone to benefit from blockchain infrastructure.

Meanwhile, transparency and security in the ecosystem are on a rip; Bitcoin’s halvening is well understood, Ethereum transitioned from proof of work to proof of stake without jargon or drama in 2022 and as chains scale through Layer 2 technologies, they are becoming increasingly stable. We can’t wait to see products that serve the non-crypto native as mainstream use cases become more apparent and ETFs bring cryptocurrency to the popular conscience.

Finally, as WorldCoin has emerged to verify human identity, we are excited by the uses of hash data to verify content for both consumers and enterprises. Blockchain and generative AI marry up in use cases where machine content is now almost indistinguishable from human content. The best way to verify a medium’s provenance might well be to add it immutably to the blockchain for anyone to check. We can’t wait to back founders building multi-purpose solutions to the many threats to media authenticity.

When we invested in WaveXR back in 2018, we had a strong belief that virtual reality will change the way people share experiences with each other. We have continued to harbour that conviction and see present moment as an especially exciting inflection point. In the 5 years following the launch of the Apple smart watch, the industry grew 1340%. We are optimistic that headsets will experience a similar if not bigger trajectory. Alternative reality hardware has existed for a long time in Hololens and Oculus and as more members of FAANG join the party, we expect use cases to explode.

One difference between headsets and other hardware like headphones or watches is that headsets are a platform. It makes sense to build on top of them and new applications to experience spaces, gamify chores and enjoy multimedia are exploding. Adjacent technologies like Gaussian Splatting and NerF will only make AR and VR more exciting as people bring incredible 3D assets and experiences into their augmented experiences. We can’t wait to back the founders building on top of these platforms to create amazing alternative universes and enliven our real one.

If you’re working in any of these sectors (or have a strong take on what else we should add to this list), we’re all ears 👂. Let us know here.

Cash flow management is the primary reason why SMBs go out of business. Business owners and financial professionals still rely on a burdensome system of financial tools to manage money transferred in and out. For SMBs outside the SaaS and e-commerce payment systems, the challenges are particularly significant.

This is why we are excited to back Mimo – which stands for ‘Money In, Money Out’ – a platform simplifying global payments, cash flow, and financial management for SMBs and finance professionals.

Founded in 2023 by CEO Henrik Grim (former General Manager of Europe at Capchase and Investment Manager at Northzone), Alexander Gernandt Segerby (CPO), and Andreas Meisingseth (CTO), the London and Stockholm-based company provides a suite of financial tools that bundles the features needed for SMBs to better understand and control their cash flow.

Mimo gives businesses, accountants, and bookkeepers a single tool for easier administration and better financial decisions. The platform’s credit offering helps minimise risk and optimise working capital, enabling businesses to send and receive payments on their own terms. Trading SMBs and finance professionals can pay suppliers with a click, access working capital, and get paid faster by customers, in any currency.

For businesses that hold inventory or trade internationally (e.g. those in consumer goods, retail, hospitality, or wholesale) and require a substantial number of invoices and multi-currency management, Mimo’s financial management solution solves the painstaking, time-consuming issues that are synonymous with these sectors.

Mimo already works with 50+ SMBs and finance professionals and processes several million GBP every month via its early access offering.

Henrik Grim, co-founder and CEO of Mimo, comments:

“I’ve seen first-hand the time-consuming and fragmented processes SMBs must deal with when managing money. SMBs and financial professionals have to jump between apps and spreadsheets to pay invoices or make and chase international payments, all while trying to keep track of and manage cash flow. Mimo bundles this into a single tool so that businesses can easily manage the movement of their money and receive payments in any currency, faster. We’re delighted to be backed by our investors to help give SMBs full control of their finances.”

On why we invested, our Partner Sia Houchangnia comments:

“We’re seeing a step-change in how SMBs are equipping themselves with technology to become more astute and proactively-minded businesses. From their work at iZettle, Hedvig, and Capchase, Henrik, Alex, and Andreas are deeply entrenched into the financial management needs of SMBs which they are now solving for with Mimo. We are thrilled to partner with them on this journey.”

We are excited to participate in Mimo’s £15.5M (€18M) funding round led by our friends at Northzone and joined by Cocoa Ventures, Upfin VC. The round also includes an asset-backed facility arranged by Fost and participation from angel investors including founders and early operators from Stripe, GoCardless, Wayflyer, and Anyfin.

Mimo aims to continue to build out its B2B payments solution for SMBs and expand its headcount which now includes 14 employees, of five nationalities, across the company’s two locations.

For more information, visit mimohq.com.

Commercial fleets represent approximately 10% of total European emissions. Playing an essential role in the continent’s green transition, there is a significant drive for sustainability and electrification of commercial fleets. However, the switch to EV-native fleet management and operations is complex, costly, and disruptive. The core of the problem lies in the fact that the commercial fleet ecosystem – from vehicle leasing to fleet operations – treats EVs like low-grade ICEs (internal combustion engine vehicles), not capitalizing upon EV’s benefits, such as their high durability and energy efficiency.

This is why we are excited to back Pelikan Mobility, a UK and France-based deeptech platform on a mission to optimize the financing and operations of sustainable commercial fleets.

Founded by David Salfati (Engie, Macquarie) and Vincent Schachter (CEA, TotalEnergies, smart-charging pioneer eMotorWerks sold to Enel) – who have a combined 30 years of experience in the fields of energy, mobility, algorithm development, and real assets finance – Pelikan aims to introduce the next logical step in shifting commercial mobility to electric vehicle (EV): tech-enabled, operations-centric leasing solutions.

Pelikan bridges EV leasing and fleet operations, driving down the cost of electrification by:

How does Pelikan work?

The company is developing a digital twin-enhanced EV-native leasing solution. It reconstructs – from readily available client data – digital twins that precisely capture each fleet’s operations, constraints, and business challenges.

The platform’s AI and combinatorial optimization algorithms enable the efficient integration of EVs and charging solutions into each fleet’s operations over several years.

To build an operations-centric lease plan, Pelikan starts from the fleet’s operational goals and constraints and computes the optimal use of each type of vehicle (ICEs and EVs, at different stages in their lifecycle) and the financing profile that matches that usage value. These usage and financing profiles are translated into a cost-effective and productive EVs lease plan.

Furthermore, the platform tracks and optimizes operations on an ongoing basis, ensuring the fleet leverages the full potential of its assets.

Pelikan Mobility’s solution is being deployed and tested with major utility and logistics players in France.

Vincent Schachter, co-founder, comments:

“Pelikan’s mission is to drive massive electrification of commercial fleets. In order to achieve this, we are convinced that a radically new approach is necessary. We started by developing our technology for usage-driven optimization and fine-tuned its capabilities with our first customers. With this initial round of funding, we will leverage it to lease cost-effective and productive EVs tailored to the context of each fleet“.

David Salfati, co-founder, adds:

“The finance world will need to deploy dozens of billions of euros every year into commercial EV assets, whilst the operations world will need to run them efficiently to power their business. Bridging these two worlds to ensure that capital flows into productive and efficient assets is going to be mission critical, and core to what Pelikan is building.”

On why we invested in Pelikan, Kate McGinn from our investor team, comments:

“The transportation sector accounts for 29% of our annual greenhouse gas emissions. Even though we have the technology to dramatically reduce this number, current leasing options are creating a bottleneck for commercial EVs to be used at-scale. As the commercial green leaser of choice, Pelikan is solving this bottleneck and challenging the way electric vehicles are financed and operated. Pelikan is finally making the green choice a pragmatic one.”

We are excited to participate in Pelikan’s €4 million funding round, alongside Pale Blue Dot, Frst, and other investors.

With the new funds, Pelikan aims to launch the leasing offer.

For more information, visit pelikan-mobility.com.

Driven by the rapid adoption of EVs across Europe, there is an increased demand for public infrastructure to provide quick and frictionless usage of charging stations to end customers.

Given the multitude of eMobility stakeholders building the EV charging infrastructure, a reliable and scalable connectivity layer is essential to provide better EV Driver experiences. Current solutions lack scalability, are expensive, and lead to poor data quality around charge point availability and charging fees.

This is why we are excited to back Enapi, a Berlin-based connectivity platform for collaboration in the electric vehicle (EV) charging industry. It facilitates connections between Charge Point Operators and entities developing and providing digital charging solutions for consumers and businesses.

Founded by Jakob Kleihues (CEO) and Dennis Laumen (CTO), Enapi is building the transaction broker and clearing house for the electric vehicle (EV) charging industry to effectively connect Charge Point Operators and eMobility Service Providers. As an infrastructure layer company, it aims to tackle the challenges of technical interoperability.

On a mission to build the most secure, reliable, and scalable platform for stakeholder collaboration in the EV industry, Enapi empowers participants in the marketplace to adopt and expand the use of open protocols, thereby enhancing community collaboration and elevating the quality of data. The Enapi Transaction Broker enables EV charging transactions, using the OCPI standard to ensure seamless charging station connectivity.

Jakob Kleihues, co-founder and CEO of Enapi, says:

“The EV charging infrastructure is broken. Enapi plays a pivotal role in enabling charge point connectivity and creating streamlined collaboration to improve the way we charge our electric cars. Enapi serves a large addressable global market of electric vehicle charging transactions, helping to deliver a better EV driver experience and thus fueling the green mobility revolution.”

On why we invested, Kate McGinn from our investment team comments:

“Over the next 10 years, we have to build out the green equivalent to our petrol station network, all the while not falling prey to copy/paste approaches which don’t take into account the intricacies of ICE vs EV. Enapi is building the unified API for EV charging and removing friction for all parties in the charging world to communicate seamlessly with each other. We’re thrilled to partner with industry insiders Jakob and Dennis on this journey.”

We are excited to participate in Enapi’s €2.5 million pre-seed round alongside Project A Ventures and HelloWorld. With the new funds, the company plans to expand its network, enhance the data quality on the platform, and build clearing house functionalities to enable charge point connectivity at scale.

Enapi launches its service today with a group of renowned partners across Europe onboarded: Electra (FR), Monta (Nordics), JUCR (GER), Osprey, Octopus Electroverse, OVO Drive, Paua (UK). Other stakeholders from the industry can join the platform by invitation or join the waitlist.

For more information, visit enapi.com.

Cybersecurity has always been a fast changing landscape, but with the rise of widespread-access AI tools such as ChatGPT, we are seeing Artificial intelligence is catalysing a paradigm shift in cybersecurity architecture. Traditional systems, designed to protect against decades of relatively stable known threat types, are increasingly inadequate against AI-augmented attacks, which can analyze vast datasets and exploit vulnerabilities at unprecedented speed and with unprecedented creativity.

Emerging challenges, such as the automated generation of sophisticated phishing attacks, which grew between 500% and 1000% YoY in 2023, or the exploitation of previously unknown software flaws which are being brought to light at volume through AI, require urgent solutions. Massive data management challenges and breaches are surging and impacting public businesses like Hubspot to security darlings like Okta. This isn’t just a risk to survival and security is no longer considered just a cost center. It is also critical infrastructure and 90%+ of businesses with poor security practices missed revenue goals last year. Even the premise behind alerts, alerts analysis and alert management is under stress due to the creative nature of attacks which can be layered and more complex than ever before.

This has prompted a wave of innovation among cybersecurity firms, focusing on adaptive, AI-centric security frameworks. These frameworks are designed to anticipate the evolving tactics of adversaries, ensuring that digital infrastructures can withstand the sophisticated cyber threats of tomorrow. Managing software access for AI agents or integrating security practices in the production and deployment of code, for example, are starting to emerge as crucial lines of defense for any organisation.

_________________________________________________________________________________________

At Seedcamp, we are aware of the above challenges and more, and thus are investing in a new stack of tooling and frameworks to stop attackers in the era of generative AI. Whereas tooling once focused on a certain element like a network, or a device, software is increasingly safeguarding the intersections and understanding the intent of both machines and humans.

To this end, our thesis is underpinned by four distinct categories:

(1) Managing identity more intelligently for humans and machine agents

(2) Shifting left in the software development lifecycle to secure code as it is written

(3) Surfacing complex fraud detection beyond simple pattern recognition

(4) Securing an organisation’s data, regardless of how it is managed in transit, at rest and in use.

In the past, access management was rules-based systems that ensured only the right people access an organization’s data and resources. Role Based Access Management (RBAC), Identity Access Management (IAM) and Privileged Access Management (PAM) were ‘top-down’ and permitted access based on an employee’s rank and function. This was typically a ‘point solution’ in the sense that it solves a single problem in a tightly defined zone of relevance.

This top-down logic is being replaced by tooling that is more context-aware and primed to handle both machine and human users. Attackers have historically snuck past identity systems by understanding the rules and logic and posing as an entity that is permissioned, i.e. by using the email address and password of an employee. Today, machine agents are accessing the same software without passwords or ‘clearance’ in a traditional sense. It is therefore imperative to understand the ‘why’ and ‘how’ behind an access request, in order to decide on what should and should not be accessed. To this end, we have invested in businesses that manage, protect and bring visibility to this evolving environment.

“AI is fundamentally changing the way companies manage their access to software: AI provides context to processes that were merely rule-based in the past. Think of user access reviews, offboarding, or time-based access – AI guides IT and Security teams with recommendations (e.g. “Julia hasn’t used Figma for 9 weeks. You can most likely remove her access.”). This not only frees IT and security teams from manual, mundane tasks but also increases your security and compliance posture.”

Johannes Keienburg, CEO of Cakewalk

Classical cybersecurity largely safeguards the end product – the ‘surface area’ is the zone in which users interact with the software. Detection happens after code has been written and shipped and prevents attacks on the application or infrastructure. Recently, tools are ‘shifting left’ in the software development cycle to automatically check the code base for vulnerabilities.

This developer-first tooling began by effectively scanning static code bases. More recently, it has become ‘real-time’ to operate in parallel with the machine or human actually writing code. To the chagrin of software developers, programming is merging with security and vulnerability scanning will inevitably be instantaneous as code is written. To generalise, these alerts are slightly ‘higher fidelity’ and can help provision resources and even prioritise the haul of alerts that security analysts currently handle.

Catching issues long before code is shipped to the enterprise is exciting and at Seedcamp we are pleased to partner with organisations who make this their mission, including:

“Security should be something developers take responsibility for in the same way they consider how to structure their application, which database to use, and how to approach writing integration tests. It’s often said that developers don’t care about security, when really they just don’t have the right tooling. That needs to change if we want to build software that is secure by design.”

David Mytton, CEO of Arcjet

Impersonation and identity theft represent an enormous threat surface area for the enterprise and for individuals. Global fraud is worth over $1 trillion and onboarding customers, businesses and employees is a huge cost-center. To verify and approve a single identity, enterprises are already deploying several different packages which might independently check KYC, AML, sanctions, political interests and more. For fraudsters, it is essentially very easy to triangulate the personal details of someone from social media and online content. The volume of attempted attacks is only likely to continue growing.

Additionally, fraud tends to be lodged in opaque spaces. Longtail personal details and identities are rarely checked, such as a reference for a job, a merchant on a food delivery platform or a guarantor of a tenancy. Hiding stolen identities or non-compliant information deep in documentation has historically been a simple way to get around checks which tend to focus on the main event – the user or customer.

At Seedcamp, we are excited to partner with businesses securing the entire enterprise workflow against fraudulent individuals and businesses. Some of the solutions we’ve backed include:

“Rising identity-based cyberattacks demand proactive solutions, making automated KYC verification vital for a more secure environment for businesses and their customers. With spektr, continuous client data monitoring, proactive alerts on profile changes, and international data screening ensure fast, secure operations.”

Mikkel Skarnager, CEO of spektr

Finally, it is no secret that organisations are losing an uphill battle to prevent data leakage. As data is plugged into language models, it is almost impossible to tackle the probability that it will escape as an output and be sent outside the organisation. The explosion of free browser based services also means that employees are uploading confidential data on a daily basis to design, content and other automated tools that may be visible to 3rd parties.

“The cybersecurity battleground is shifting. While traditional tools such as perimeter defenses are still important, they don’t work for the large and constantly growing attack surfaces that Generative AI exposes to enterprises. The first line of defense is the application developer. At Bookend we’re building for a future where developers can quickly and simply protect applications from Generative AI-related threat vectors that cause model misbehavior, and focus instead on empowering their organizations to innovate more rapidly.”

Pravin Pillai, CEO of Bookend AI

New tools are emerging to tackle this problem and the process of tracing data and keeping it squarely within an organisation’s four walls is just beginning. Where security was previously one-size-fits-all, it will need to intensify at certain intersections to prevent issues like toxicity and shield employees from a growing wave of fake AI-driven messaging and content.

We are excited about the companies we have partnered with to bring transparency, collaboration and trust to data in the enterprise:

“The old paradigm for data security treated it as atomic pieces of information. With the rise of Large Language Models (LLMs), Natural Language Processing (NLP), and evolving AI/ML techniques, the challenge of data security has now shifted to the level of Knowledge Management which derives meaning from the data we once tried to protect. The paradigms of the old model do not translate well or scale to the new model and we have to find a more effective path than trying to persist the illusion of having our arms around the atomic information.”

Nick Vigier, CISO of Oscar Health*

_____________________________________________________________________________________

The security landscape is evolving rapidly and we are actively trying to solve how best to protect our valuable information infrastructure. If you are a founder of an early-stage security startup, we would love to hear what you’re building!

*Not a Seedcamp portfolio company

Regulatory and technological tailwinds drive investment decisions and as we look ahead, we are excited about emerging catalysts for the software stack and for society. In this article, we touch on just some of the solutions we think might change the world in the next 17 years.

Above all, the demands of our warming planet, chronic disease and disorganised digital environments are in need of software solutions more than ever. Although we can’t wait for a bitcoin ETF to propel decentralised applications and WebTransport and WebGPU to unlock instantaneous, collaborative and high quality entertainment experiences, here we focus specifically on the future of critical infrastructure across security, climate and techbio.

Security

It’s no secret that our digital and physical worlds are changing and we need new software to make them sufficiently secure. So far in Fund VI, we have backed Enzai, Arcjet, Spektr, Bookend, and others still in stealth mode, and look forward to more outstanding opportunities.

The elephant in the room is that generative AI creates immense data risks and we are faced with myriad known unknowns. For example, we haven’t figured out identity control for AI agents that operate software autonomously, access management to company data that can be queried by anyone and open source model safety, whose output is almost untraceable to training data.

In our cybersecurity portfolio deepdive we focus on these emerging challenges and how our portfolio is primed to support enterprises and capture value.

Climate

Elsewhere in sectors like climate and cleantech, we combine a distinctive track record with strong conviction about why the time is right. Seedcamp has supported THIS and Julienne Bruno on their journeys to become two of Europe’s fastest growing plant-food brands, while Papaya, Granular and Sylvera are emerging as early leaders across EV fleet management, energy market solutions and carbon data. We are also especially excited about vertical fintech in clean energy and we look forward to the journeys of Paua and other unannounced commitments driving optionality and flexibility for early adopters.

Over the coming years, we anticipate the emergence of infrastructure that will power a clean and efficient energy system. Be that software that drives a smarter grid and better load-balancing, connected batteries that avoid discharging at times when their operating costs exceed the price of energy or intelligent, local procurement to avoid sending energy hundreds of miles on lossy lines across a continent with thousands of grids and DNOs. At smaller scales, we see the interaction of sensor technology, the Internet of Things and edge-based machine learning dramatically improving industrial energy consumption. Currently, usage is ungovernable and expensive. We anticipate a future where top-line energy consumption doesn’t necessarily need to be pared back, but we can access data and understand usage far more intelligently.

Techbio

Finally in techbio, we look forward to being part of the software-enabled future of drug targeting and discovery. We have already backed businesses like Inovia Bio, Twig Bio and Sable Bio, Lindus Health in clinical trialing, and Faks at the other end of the supply chain in drug delivery. In the coming decade, we see a wealth of opportunities throughout the biomedicine stack; to research and develop treatment for chronic infections like SARS-CoV-2, to anticipate and prevent target failures, and to build the molecules needed for food without meat and plastic without petrochemicals.

Research at the intersection of biology and computing is also primed for a tipping point. Businesses like Apoha are driving sensory intelligence and we anticipate many more use cases of unconventional or neuromorphic computing architectures and even substrates that reflect the brain’s qualities.

For example, rather than the input-output systems of deep learning where training and inference are essentially separate chronological activities, a continuous state machine similar to the human brain’s operating system, would enable a network to evolve around changing parameters, perhaps even paving a route to AGI. Elsewhere we could even see storage based on biology’s principles – a single gram of DNA is worth 200 terabytes – and active inference techniques allowing drones and robots to deploy the sensibilities of a person. We think Retrieval Augmented Generation and NLP applications are exciting but we also can’t wait to see the impact of machine learning on life-saving science, and vice-versa.

_________________________________________________________________________________________

Of course, techbio, security and climate are just a few of the sectors where we think software has enormous potential to disrupt the next decade. Evolving categories like vertical-market software, blockchain infrastructure, database management systems and many more are at the top of our agenda, in addition to more mainstream sectors like fintech, which are yet to fully penetrate society. At Seedcamp our world class in-house experts cover almost every sector and job function, helping entrepreneurs steer the ship, evangelize the product and raise impactful rounds on the way to becoming a category-defining business. As ever, we are always on the lookout for Europe’s strongest founders at the start of their journey–if that’s you, please get in touch on our website or reach out to any member of the team!

If you missed the previous two installments of this series, catch up here and here.

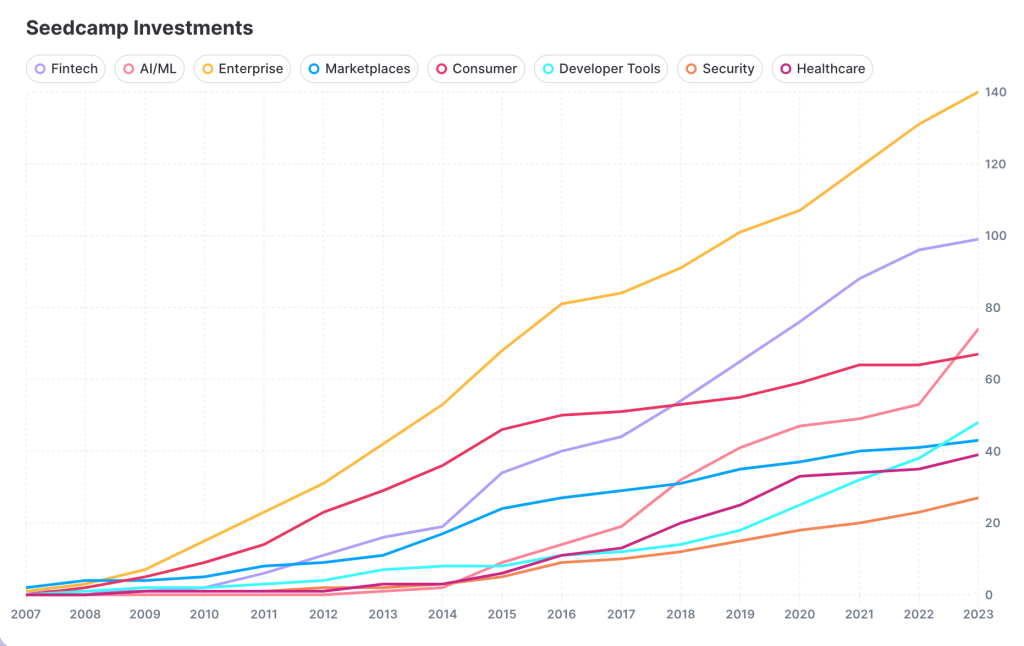

Each Seedcamp vintage tells a unique story about the tailwinds and themes behind our investment decisions. We think that venture is about seeing the present for what it is and committing to founders on missions to solve deeply painful problems. The most exciting solutions are unorthodox and start on the very edge of markets before gravitating to the centre. We invested in Revolut long before mobile banking reached the masses, in Grover when the circular economy was in its infancy and Synthesia when no one had heard of generative AI. In our second installment celebrating the Seedcamp Nation’s milestones, we wanted to share some of the threads that weave together our investments in no-brainer products, inefficient markets and extraordinary entrepreneurs.

Timing matters and we make it our business to understand fast-moving currents before they reach escape velocity. For example, we lent into fintech in 2015 as open- and neo-banking came to market and our AI commitments accelerated around key breakthroughs– TensorFlow in 2014, Transformers in 2017, and GPT-4 in 2022. As different forces emerge, our theses evolve, resulting in distinctive waves of investment tracing back to 2007.

The total companies invested exceed the number of Seedcamp Investments, as some companies are in more than 1 sector (max 2). Made with Graphy

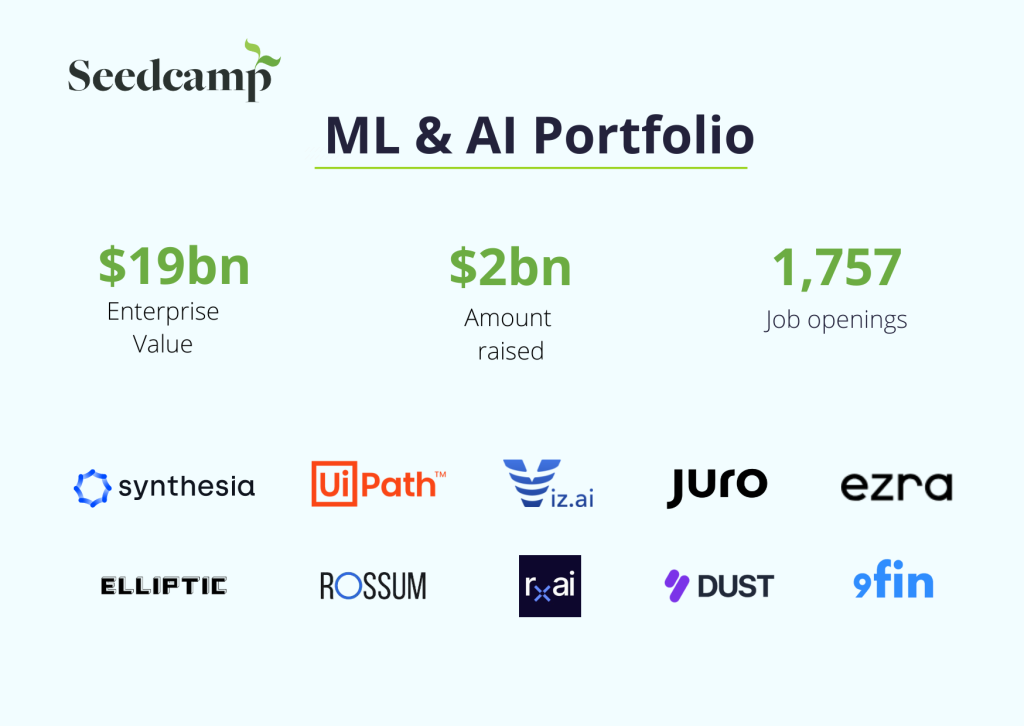

Machine learning first caught our attention in 2012 when we backed Charlie Finance and then Elliptic. Since then, we have invested across the infrastructure and application levels, watched UiPath (NYSE: PATH) go public and recently cheered on Synthesia to unicorn status in one of Europe’s rare growth rounds of 2023. It’s a sector we have studied for over a decade and we can’t wait to see commitments in the enterprise stack like Juro and Rossum continue their upward trajectory, while pattern detection technology like Viz and 9fin drive discoveries across healthcare and finance. Of course, we couldn’t not mention that as GPT-3, -3.5 and -4 have blossomed, we have been thinking about what LLMs will mean and how they will be used in the enterprise. We have made investments like Dust and AskUI to drive business processes, but also can’t wait to see what this technology means for biology, medicine and chemistry. Many components of the machine learning stack like devops, guardrails and security are just getting started and we look forward to supporting the leading minds.

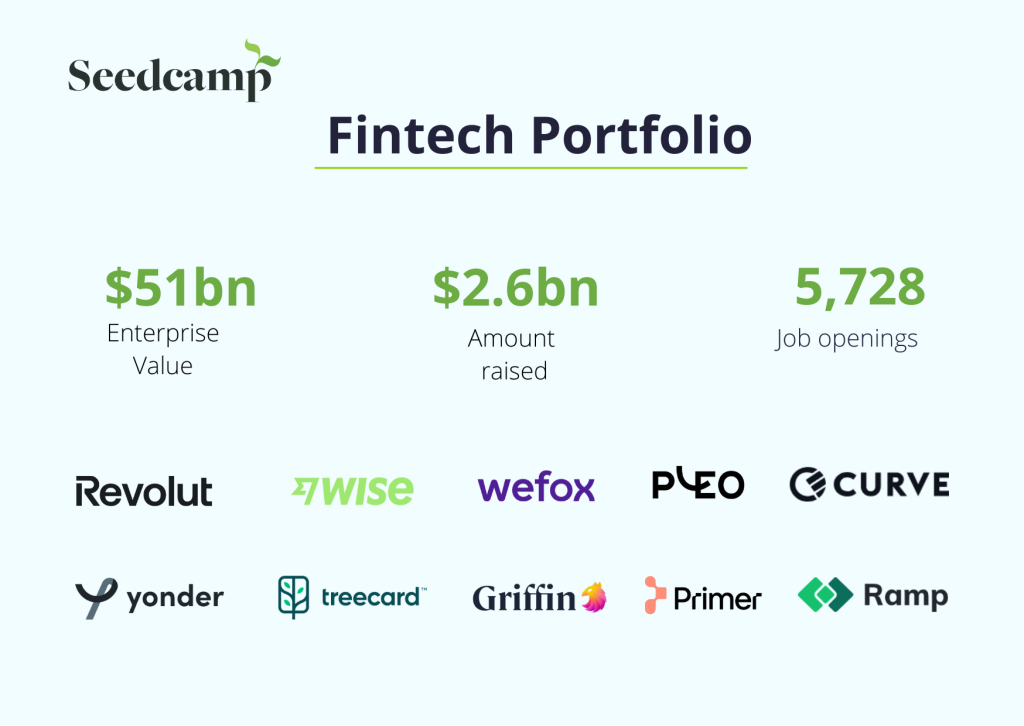

Around the same time as the first wave of machine learning startups emerged in Europe, financial technology began to catch our eye. We came with a prepared mind in 2011, when we invested in Taavet and Kristo’s mission at Wise (LSE: WISE) out of Fund II. In Fund III we were among the earliest supporters of unicorns Pleo, WeFox and Revolut, which recently announced revenue expectations of $2bn for 2023. Meanwhile, other members of the Seedcamp fintech portfolio are in the earlier years of their journey. On the consumer side, Yonder and Treecard are revolutionizing credit and impact at a rate of knots, while Griffin, Weavr and Primer break new ground in the worlds of embedded finance and payments. Financial digitalisation is still in its first innings and while fintech accounts for less than 10% of global transaction volume, we look forward to supporting the next wave of technology that fixes the broken worlds of banking, real-estate, payments, procurement and much more.

In spaces that are a little earlier – like open-source – we think we are where fintech was in 2016

Of course not all themes align neatly to sectors. For example, Adobe’s Flash Player accelerated the development of multimedia applications across all industries and the platform shift to mobile gave rise to innovation from gaming to the Internet of Things. In our emerging portfolio, open-source business models stand out as a fundamental shift in go-to-market philosophy, away from the ultimate buyer in the finance department, and towards the developer. Two rapidly growing businesses that have struck a chord with programmers are Appwrite, which raised its Series A from Tiger Global for its backend in-a-box and Meilisearch, which raised an A round from Felicis for its embedded search engine API. While some open-source commitments look like conventional developer tools for optimizing the process of code writing, deployment and release, others look more like Saas that is simply developer-first. Baserow is a no-code database built in Django and Nust, Rerun is an SDK for visualizing multimodal data, and Medusa is a platform for building rich performant commerce applications. As more and more open-source companies transition their fanbase to paid and supported services, we are excited to see these businesses flourish.

_________________________________________________________________________________________

For any startup looking to build something truly awesome, Seedcamp is the place to start.

Taavet Hinrikus, Co-founder of Wise

Each year, new ideas emerge around fresh ways to build and sell software products. It has been a privilege to partner with businesses on various journeys, from on-prem to the cloud, from desktop to mobile, from centralised to decentralised, and more. Today, new tools are enabling everyone to be a developer, application UX is increasingly voice-first and infrastructure is enabling data to be ingested, transformed, loaded, streamed and analyzed with incredible efficiency. We can’t wait for what’s to come and in episode 3, we look ahead to the next decade.

If you missed Part I, read it here: Seedcamp Turns 17. The Seedcamp Nation and the European Tech Ecosystem, Then and Now (1/3)

Also read Seedcamp Turns 17 | The Next Decade (3/3).

Copyright © 2019 Seedcamp

Website design × Point Studio